Medically Reviewed by Dr. Hossain Licensed Mental Health Professional sychotherapy, particularly trauma-focused modalities Medical Director

This article is for informational purposes only and is not a substitute for professional medical or legal advice about your specific insurance plan. If you are in crisis, call or text 988 (Suicide & Crisis Lifeline) or call 911.

The Short Answer

Yes — in most cases, your insurance is legally required to cover mental health treatment in New Jersey, including therapy, Intensive Outpatient Programs (IOP), and Partial Hospitalization Programs (PHP), on the same terms as any physical health condition.

But “covered by law” and “an easy, fully-paid experience” are not the same thing. Coverage still depends on your specific plan, whether your provider is in-network, and whether the treatment is documented as medically necessary. This guide breaks down exactly how that works in New Jersey, what can go wrong, and how to find out your real numbers in under 20 minutes.

Don’t want to read the legal fine print? Skip straight to the answer. Call

(609) 293-3481 or verify your insurance online and our admissions team will tell you your exact coverage — no cost, no obligation, usually within one business day.

Why This Question Keeps People Stuck

According to the National Alliance on Mental Illness, roughly 1 in 5 U.S. adults experiences a mental health condition in a given year — yet a large share delay treatment for months or years, and insurance confusion is consistently one of the top reasons cited. Not fear of stigma. Not lack of access to a provider. Simple uncertainty about the bill.

That gap between needing help and asking for help is where treatment outcomes are won or lost. The sooner someone gets an accurate answer about cost, the sooner they can actually start.

“Insurance confusion is one of the most common reasons people delay treatment for months or years — not because they don’t want help, but because they don’t know if they can afford it. Verification takes minutes. Waiting in uncertainty can take years off someone’s recovery timeline.” — Dr. Hossain Licensed Mental Health Professional sychotherapy, particularly trauma-focused modalities Medical Director at True Life Care Mental Health

The Legal Foundation: Why Insurers Have to Cover This

Three layers of law work together in New Jersey:

- The federal Mental Health Parity and Addiction Equity Act (MHPAEA) requires insurers to cover mental health and substance use treatment under the same terms as medical or surgical care — no stricter visit limits, no higher copays, no tougher prior-authorization rules just because the diagnosis is behavioral instead of physical.

- The Affordable Care Act (ACA) classifies mental health and substance use disorder services as essential health benefits, which ended lifetime and annual dollar limits on this kind of care and barred denials based on pre-existing conditions.

- New Jersey’s own parity law (A2031/S1339), signed in 2019, goes a step further by requiring insurers to report on their compliance and giving the state’s Department of Banking and Insurance more power to enforce it.

On paper, that’s a strong safety net. In practice, there’s a gap worth knowing about before you assume everything will be seamless.

The Nuance Almost Nobody Tells You

New Jersey’s parity protections exist — but enforcement of them does not always keep pace. In its 2026 state-by-state analysis, ParityTrack gave New Jersey an “F” grade for parity enforcement, despite the state having one of the larger insurance markets in the country. Separately, federal regulators told a U.S. District Court in March 2026 that they would not defend the current MHPAEA enforcement rule while a revised version is drafted, with a new rule expected by the end of 2026. On the ground, a federal Department of Labor review found that the single most common parity violation was insurers requiring prior authorization for therapy sessions that they didn’t require for comparable medical visits.

None of this means your insurance won’t cover treatment. It means the law is on your side, but the burden of catching a wrongful denial or an unnecessary prior-authorization hurdle often still falls on you — which is exactly why a proper benefits verification, done by people who do it every day, matters more than reading your policy PDF alone.

What “Medically Necessary” Actually Means

This is the real gatekeeper, more than the insurance company’s name on your card. Coverage isn’t triggered just because you want treatment — it’s triggered because a clinician documents that a specific level of care is clinically appropriate for your symptoms.

That’s determined through a brief clinical assessment, not a guess. It typically looks at:

- Severity and duration of symptoms

- Whether outpatient therapy alone has already been tried and hasn’t been enough

- Safety risk and daily functioning (work, school, relationships)

- Any co-occurring conditions, like substance use alongside anxiety or depression

Real-life example: Sarah, 34, works in marketing and lives in Morris County. She’d been in weekly therapy for anxiety for eight months, but panic attacks were now happening at work several times a week. She assumed IOP — a bigger commitment — would mean a bigger, scarier bill. When she called to verify her benefits, the admissions team completed a short clinical screening the same day. Because her symptoms had escalated despite consistent outpatient therapy, IOP met her insurer’s medical necessity criteria, and her plan covered the substantial majority of the cost. Her out-of-pocket portion was a fraction of what she’d feared.

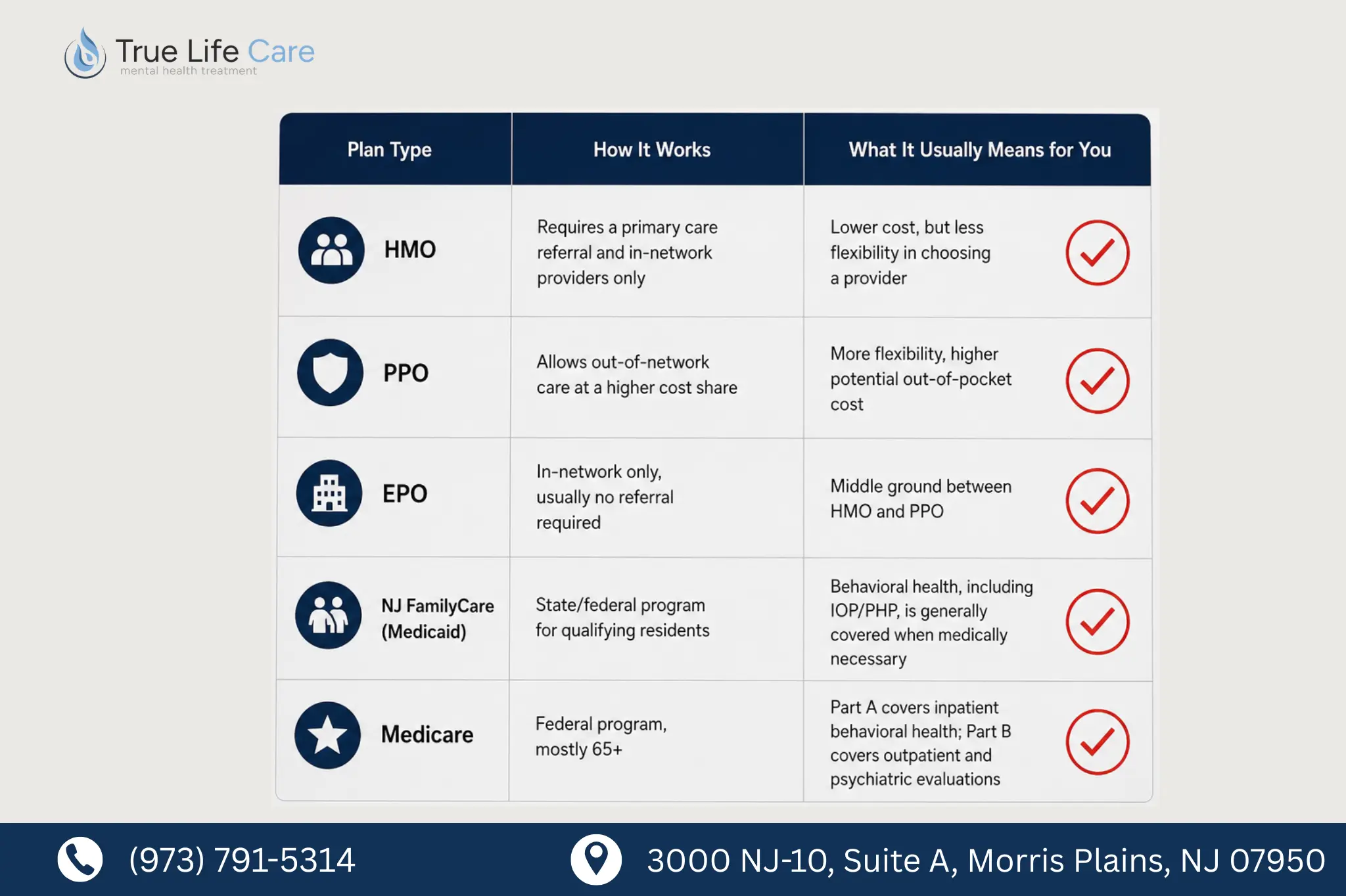

Types of Coverage: What Changes Between Plans

| Plan Type | How It Works | What It Usually Means for You |

|---|---|---|

| HMO | Requires a primary care referral and in-network providers only | Lower cost, but less flexibility in choosing a provider |

| PPO | Allows out-of-network care at a higher cost share | More flexibility, higher potential out-of-pocket cost |

| EPO | In-network only, usually no referral required | Middle ground between HMO and PPO |

| NJ FamilyCare (Medicaid) | State/federal program for qualifying residents | Behavioral health, including IOP/PHP, is generally covered when medically necessary |

| Medicare | Federal program, mostly 65+ | Part A covers inpatient behavioral health; Part B covers outpatient and psychiatric evaluations |

Commonly active carriers in New Jersey’s individual and employer markets include Horizon BCBSNJ, Aetna, Cigna, AmeriHealth New Jersey, and UnitedHealthcare. All are subject to the same federal parity requirements — but the specific deductible, copay, and in-network provider list still varies plan by plan, even within the same carrier. (Editorial note: confirm and list here which carriers True Life Care is currently in-network with, rather than implying acceptance of all of the above.)

Key Insurance Terms, Defined Plainly

| Term | What It Means | Example |

|---|---|---|

| Deductible | What you pay out-of-pocket before insurance starts covering costs | $1,500 deductible = you pay the first $1,500 of care yourself |

| Copay | A fixed fee per visit | $30 copay per therapy session |

| Coinsurance | A percentage you pay after the deductible is met | 20% coinsurance on a $150 session = you pay $30 |

| Out-of-pocket maximum | The most you’ll pay in a plan year before insurance covers 100% | $4,000 max = insurance covers everything beyond that |

| Prior authorization | Insurer approval required before treatment starts | Common for IOP/PHP; a frequent source of delay if not handled correctly |

| Medical necessity | Clinical justification required for coverage | Documented through an intake assessment |

Does Insurance Cover Each Level of Care?

| Level of Care | Generally Covered? | What Typically Determines Approval |

|---|---|---|

| Outpatient therapy | Yes, almost universally | Standard behavioral health benefit |

| Intensive Outpatient Program (IOP) | Yes, when medically necessary | Symptoms not fully managed by weekly therapy alone |

| Partial Hospitalization Program (PHP) | Yes, when medically necessary | Symptoms significantly impacting daily functioning; often a step up from IOP or step down from inpatient |

| Inpatient / residential | Yes, when medically necessary | Safety risk or inability to function without 24-hour support |

Continued coverage at IOP or PHP levels often isn’t a one-time approval — insurers may periodically review progress notes to confirm the level of care is still clinically appropriate, which is why treatment teams document progress throughout your stay.

What Can Go Wrong (and What to Do About It)

Even with strong parity laws, real friction points exist. Knowing them in advance means you won’t be blindsided:

- Prior authorization delays. This is the most commonly cited parity violation nationally. A dedicated admissions team that handles verifications daily can usually catch and resolve this faster than an individual calling alone.

- Out-of-network surprise costs. If your chosen provider isn’t in-network, your plan may still offer partial reimbursement — but at a meaningfully lower rate, and often with a separate, higher deductible.

- “Non-quantitative treatment limitations.” This is the legal term for coverage restrictions that aren’t a simple visit cap — things like unusually strict documentation requirements applied only to behavioral health claims. NJ law explicitly restricts these, but they can still surface in practice.

- Denials based on medical necessity disagreements. If a claim is denied, you have the right to appeal, and treatment centers experienced with NJ insurers can often submit clinical documentation that overturns an initial denial.

Real-life example: The Torres family called on behalf of their adult son after his depression symptoms worsened following a job loss. Their insurer initially denied PHP, approving only outpatient therapy. The admissions and clinical team submitted additional documentation showing that outpatient care alone hadn’t stabilized his symptoms. The denial was reversed on appeal within eight business days, and PHP was approved.

What Verifying Your Insurance Actually Looks Like

| Step | What Happens | Typical Timeframe |

|---|---|---|

| 1. You reach out | Call, text, or submit the online insurance verification form | 5–10 minutes |

| 2. We contact your insurer | Admissions confirms your specific plan’s behavioral health benefits | Same business day, often within a few hours |

| 3. Brief clinical screening | A short conversation to understand your symptoms and history | 30–45 minutes |

| 4. You receive a clear breakdown | Deductible remaining, copay/coinsurance, and estimated out-of-pocket cost | Within 24–48 hours of your call |

| 5. You decide when to start | No pressure, no obligation — the information is yours either way | As soon as the same week, if you’re ready |

Ready to see your actual numbers instead of guessing?

Verify your insurance online or call (609) 293-3481 Our team handles this every day — you don’t have to translate your policy yourself.

Frequently Asked Questions (FAQs)

Q. Does insurance cover IOP (Intensive Outpatient Program)?

Yes, in most cases, when a clinical assessment shows it’s medically necessary — typically when weekly outpatient therapy hasn’t been enough to manage symptoms.

Q. Does insurance cover PHP (Partial Hospitalization Program)?

Yes, generally, when symptoms are significantly affecting daily functioning and a higher level of structured support is clinically indicated.

Q. How many therapy sessions will my insurance cover?

Under federal and New Jersey parity law, insurers can’t apply a stricter visit limit to mental health care than they apply to comparable medical care. Your specific plan documents will list any numeric limits, but most comprehensive plans don’t cap medically necessary care at an arbitrary number.

Q. Can my insurance company deny mental health treatment?

Yes, a specific claim can be denied — usually over a medical necessity disagreement or missing documentation — but you have the right to appeal, and many denials are successfully reversed with additional clinical information.

Q. Does NJ FamilyCare (Medicaid) cover mental health treatment?

Generally yes. NJ FamilyCare covers behavioral health services, including higher levels of care like IOP and PHP, when medical necessity criteria are met.

Q. What if I don’t have insurance, or my insurance won’t cover treatment?

Ask about self-pay rates and payment plan options directly — many treatment centers, including True Life Care, can discuss flexible arrangements so cost doesn’t become the reason someone doesn’t get care.

Q. What’s the difference between in-network and out-of-network coverage?

In-network providers have a negotiated rate with your insurer, usually meaning lower out-of-pocket costs. Out-of-network care may still be partially reimbursed on PPO plans, but typically at a lower percentage and a separate deductible.

You Don’t Have to Figure This Out Alone

Insurance language is confusing by design, and for something as personal as mental health treatment, that confusion can be the difference between reaching out today and waiting another six months. New Jersey law puts real protections behind you. The fastest way to know exactly where you stand is to let someone check for you.

Call

(609) 293-3481 or verify your insurance in minutes — free, confidential, and no obligation to move forward.

Continue reading:

- PTSD Symptoms Checklist: When Trauma Requires Professional Treatment

- Our Intensive Outpatient Program

- Our Partial Hospitalization Program

Sources

- U.S. Congress, Paul Wellstone and Pete Domenici Mental Health Parity and Addiction Equity Act of 2008

- New Jersey A2031/S1339, official bill text via NJ Legislature

- Office of the Governor of New Jersey, press release on mental health parity enforcement legislation

- ParityTrack, New Jersey state parity report

- MoneyGeek, “Mental Health Parity Laws by State 2026”

- NAMI New Jersey, mental health parity advocacy